Let’s find out how the first Ukrainian mobile-only bank monobank succeeded

Today, neobanks (mobile-only banks) are growing in popularity. Maybe ten years ago it would have seemed impossible, but today they are already competing with our traditional banks. A striking example of such a phenomenon is Ukrainian monobank. The bank attracted more than 1.5M clients in two years, and provided loans amounting to no less than $270M, which seems to be an impressive result for just two years of work.

Oleg Gorokhovsky, who is the cofounder of monobank, tells us about the competition, successful products, fails, plans for the future, and the Koto project in an interview with PaySpace Magazine.

Interview with Oleg Gorokhovsky, the cofounder of monobank

You launched monobank two years ago, in November 2017. How many people use the app today? What about deposits, loans, and cashback?

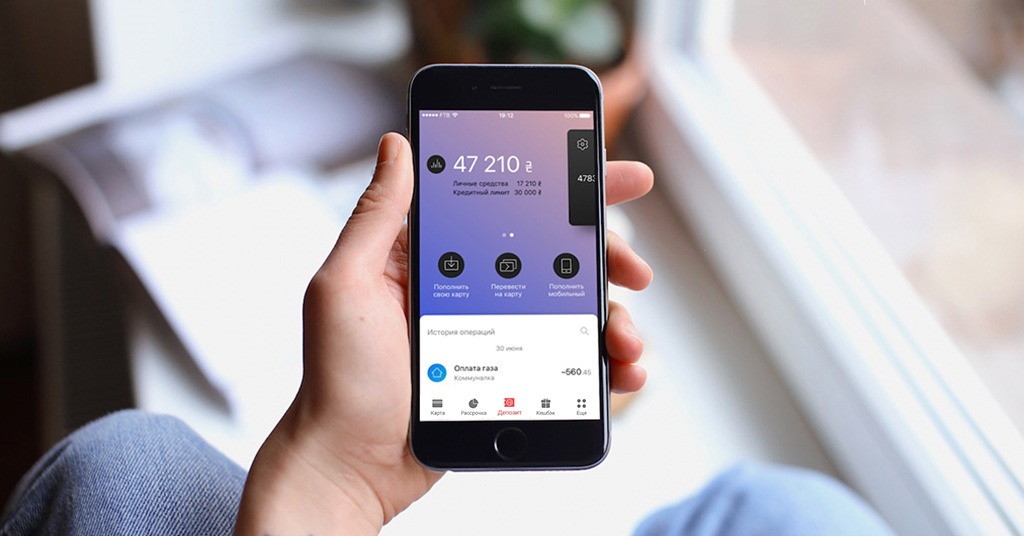

Today, we have 1.5M users, which attracted deposits totalling $230M. Moreover, our loan portfolio is about $270M. After all, we paid more than $19.2M in cashback.

Can you already call your project successful? If so, what is the secret of monobank’s success?

Yes, we have definitely managed to create a bank that clients love. I think our success consists of three key components:

- A simple product with moderate fees and a convenient app.

- Emphasis on pleasant experience and emotions when interacting with the user.

- A cool and motivated team, which is developing the product and solves all the service-related issues.

However, we are not going to rest on our laurels. It is important to work hard every day if you want to maintain the status of a successful bank.

Our major aim is to reach the 5M clients mark by the end of 2022.

Tell us about the most popular services of monobank. Maybe some products have failed?

The latest thing is the section where users collect awards for the active use of our services. This is a cool thing that sets us apart from other banks and reflects our emphasis on the emotional component of service. Let’s consider some statistics:

- 838,000 users are involved in the collecting process

- 85,000 clients visit their rewards pages daily

- In total, clients collected approximately 1.5M awards

The first thing that pops into my mind when I hear failure is the “Sport deposit”. We made a bet (or kind of) with our depositors: if they took 10,000 steps a day, we increased the percentage rate of their deposit. On the other hand, those who did not fulfil this condition faced the opposite situation – we decreased the percentage rate of their deposit. Some users gave up after a couple of unsuccessful attempts, but some clients managed to cheat. They used special pedometers and hacked smartwatches in order to increase the number of steps. Most “hackers” added steps during the night, and we called them “nightwalkers”. Eventually, we gave up on this type of deposit, and abandoned it.

Who is your target audience?

We have a fairly young audience: the majority of clients are under 35 (around 1M users). Only 10,000 clients are over 65 years old. According to our data, half our clients have a higher education. Now about professions: the most common occupations are in the field of trade and IT. Almost 70% of customers live in cities with a population of over one million people. 66% of customers use Android, while 33% use iOS.

How many users do you plan to attract before your audience’s growth will slow down?

As I’ve mentioned before, our major aim is to reach the 5M clients mark by the end of 2022. But it’s too early to talk about market exhaustion – according to GFK, today 17.7M adult smartphone users live in Ukraine.

Tell us about the card for children that you plan to launch. Do you believe it is necessary to develop financial literacy among children and young people?

Different banks create multiple youth financial literacy programs and consider them as major educational programs. We do not pursue this idea. We just create a cool banking product for kids.

Children desire to imitate their parents, and banking deals (card payments, bill payments, etc) is a part of the game. They want to feel like adults, so they want to use bank cards just like adults. Therefore, the monobank children’s card will be exactly the same as the adults’. According to law, children cannot own a card and independently use funds. Thus, it will be a children’s card with parental control.

You have launched platinum cards without a number, CVV2, and expiry date. You also claim that this is a new stage in the development of the payment industry. Is it possible that someday a plastic card will become a vestige of the payment industry?

Plastic cards are being called “a vestige” or “unnecessary things” for a long time, but are still in demand.

But it would be fair to note that now we have a lot of customers who have never used plastic cards. Anyway, it is hard to predict what will happen to plastic cards.

Tell us about the target audience of Iron Bank and all the benefits of this product.

This is a product for VIP customers. The client receives a card made of metal, which is three times heavier than an ordinary card. This card includes a 24/7 concierge service; air miles program; free access to airport business lounges in 450 cities around the world; Fast Line in the departure and arrival areas; branded application with a modified interface and additional (loyalty program) options.

We issued 2,300 iron cards in 2018. It is a kind of a “posh” option, so it is not as popular as, for example, the platinum card (with more moderate fees).

What about your products for entrepreneurs?

We have already created a design team and begun product development. Our aim is to create a simple modern product for entrepreneurs. It is too early to speak about the specific date, but we are striving to launch the first version of the product in the first quarter of next year.

What payment instruments are especially popular among Ukrainians, and why does it happen this way?

I would especially like to note money transfers through the contacts book if we are talking about monobank. This is very convenient because you do not need to know the user’s card number and worry that you have made a mistake while typing this particular number.

But if we are talking about the entire market, then I would single out payments through Apple Pay and Google Pay.

Do you think that the launch of monobank has given impetus to the development of the banking market, and will Ukrainian banks massively launch similar neobanks?

Of course, we note that projects with a similar business model will appear on the market. Some Ukrainian banks will launch their neobanks soon.

We are not against the competition, but I believe that just starting a neobank without completely rethinking the classic/conventional approach and experience of a client-bank interaction is not the right solution.

Under what conditions can European neobanks (N26, Revolut, Monzo) enter Ukraine? Will such banks be popular here?

I believe some of these banks are interested in this market. For example, Revolut has already announced its launch in Ukraine. Well, it is not yet clear under what conditions Revolut will enter the Ukrainian market, since you need a license from the National Bank in order to run a fully-fledged banking activity here, which is not so easy to obtain.

But, be that as it may, we are ready for the new competitors. Recently, we have added a new bill-splitting feature. Revolut already has such a feature, and we believe that such healthy competition will “keep us in shape”.

We’ve heard that European neobanks appear to be unprofitable. Is monobank already profitable?

Yes, the bank began to turn a profit in January 2019.

Which banks (possibly foreign ones) can be a good role model?

It is very important to keep track of other players. Not just for the purpose of imitation, but to understand in what direction the industry is developing. We regularly monitor neobanks, in particular – Revolut, Monzo, N26, Monese, Tinkoff Bank.

Tell us about the financial license application in the UK. Was it difficult, and how much time did you spend on this?

Yes, this is quite a difficult process. Firstly, the British market is rather regulated and doesn’t want to see new players on the market. It took almost a year and a half to get a license.

Secondly, you should consider the cultural differences between Ukrainians and the British. However, we have accomplished all the bureaucracy-related processes, so we are only a few steps from the launch of our product.

When do you plan to launch Koto? Why did you choose this country? How do British preferences for banking products differ from the preferences of Ukrainians?

Now we are testing the product in the “Friends & Family” format, and the general release will be in November or December. We look forward to a successful launch.

We believe you can already compare the banking markets of Ukraine and the UK in terms of technology. Is Ukraine lagging far behind?

Perhaps I will surprise you, but we are not lagging too far behind. On the contrary, for some indicators, we are even ahead of Western markets in terms of technology. For example, we were second, after Apple, to issue a card without a number. Moreover, Ukrainian Alfa Bank also issued one right after us.

This can be justified by the fact that banking in Ukraine is a relatively new phenomenon, unlike in England, where the first card was issued more than 50 years ago. Introducing something new is always easier than refurbishing and modernising something old. Therefore, we are already used to the situation where foreign partners are stunned and surprised while looking at our technologies at monobank. We have instant freeze/unfreeze of a card, change of PIN and Internet limits, a dynamic CVV code, payments for Internet purchases without entering passwords and much more.

Are you considering any other countries to launch your product in?

We are interested in the Polish market, primarily because of the large number of Ukrainians (there are more than 2M people).

It is too early to talk about creating an individual bank there, but we will create services for simple money transfers for immigrants based on the monobank platform. As a first step, we have already launched the card in zloty (PLN), and now we are working on currency exchange and simple cash replenishment in Poland.

What technologies have most influenced the development of the banking market in Ukraine?

I would note two major solutions:

- The ability to pay for public transport by bank cards (for example, in the Kyiv subway). We’ve noticed that when a client makes frequent but small purchases with cards, card payments become some a part of their comfort zone. Thus, they get used to cashless payments (in stores, cafes, gas stations, etc).

- Apple Pay and Google Pay wallets became a real breakthrough technology that allows you to shop without having a card with you.

Which technologies can become popular in the coming years?

First, it will probably be remote authentication. Now, you need to meet with the bank representative in person in order to open a bank account. You’ll have to sign the papers and show that you are you. In my opinion, everything is ready for the accounts to be opened remotely, while the cards could be sent by mail. This should give a significant impetus to the penetration of financial services among the population. This is especially true for small cities and towns where traditional banks see no reason to open branches.

Second, it is about electronic checks, which will allow banks to see not only the purchase amount, but also the list of purchased goods. This will allow banks to build a more accurate analysis of how much money the client has spent on food or clothing. Therefore, you can open new cashback options that will fit this very client.

Are you considering a partnership with banks other than Universal Bank?

I believe we will consider it, but definitely not in Ukraine. Maybe it can be possible with Koto, but not at this stage.

One of the key figures (Dmitriy Dubilet) has left the project and gone into politics. Has it made your job more difficult?

Dmitriy has done a lot of work, especially if we are talking about the British project Koto. Without his energy, it has become harder to work. We have lost a smart partner. But we just keep going. Products and services are launching at the same speed, and we are approaching the 5,000 new customers per day mark.

Do you also plan to come into politics?

Never say never.

SEE ALSO: