Embedded finance has immense potential for the payments industry and enormous revenue opportunities for software platforms and enabling infrastructure providers

Embedded Finance Will Revolutionise Payments. Source: shutterstock.com

Merchants today may rarely if ever interact with conventional banks. At the same time, they can still open a deposit account, order a debit card, and meet most of their financing needs. How is that possible?

Small businesses prefer seamless and one-stop solutions from their e-commerce or accounting platforms. These software companies partner with banks and tech providers to embed financial products into a single customer experience.

Benefits of embedded finance

One speaks of embedded finance whenever non-financial companies offer financial products and services. For example, travel companies may provide airline credit cards or car rental insurance, while e-commerce websites offer payment plans for high-priced items. The latter is enabled by third-party ‘banking-as-a-service’ companies that use API integrations.

Solutions like that greatly simplify the lives of end consumers. That also has a positive impact on businesses that adopt embedded finance solutions. According to Plaid’s recent report, 88% per cent of companies that implement embedded finance witness increased engagement, while 85% say that it helps them acquire new customers. As a result, such solutions open up new target markets and improve customer satisfaction levels.

In 2020, a16z argued that SaaS businesses could increase revenue per customer by up to five times with embedded finance, and this prediction remains close to reality.

Therefore, embedded finance use has surged lately, and is expected to exponentially rise in the near future. Although some market leaders are already emerging in the space, incumbents and new entrants still have time to claim their share of the dynamic embedded finance market.

Types of embedded finance solutions

There are a few embedded finance types that non-financial companies may provide. These are:

- embedded banking solutions – also referred to as “banking as a service” (BaaS), allow non-financial players to offer branded checking accounts to hold funds and make payments;

E.g. Lyft offers a checking account and associated debit card exclusively to its drivers

- embedded payments – platforms can connect and save customers’ payment methods for later use at the click of a button;

E.g. the Starbucks app saves users’ payment details to power one-click purchases

- branded payment cards – any business that offers embedded banking can supply it with a branded debit card for consumers, employees, vendors, or contractors;

- embedded lending – enables companies to offer simple and favourable loan options (such as BNPL) at the point of sale;

- embedded insurance – digital marketplaces facilitate insurance purchases, while fintech companies enable consumers to choose insurance at the checkout as an ‘add-on’ to their purchase.

Source: ibtmevents.com

Market opportunities for embedded finance

Embedded finance is an emerging trend that has huge untapped potential. The research from Bain & Company and Bain Capital forecasts that revenue opportunities for embedded finance software platforms and enabling infrastructure providers will soar to $51 billion in 2026. In 2021, embedded finance revenues reached $20 billion in the United States alone, according to McKinsey.

Meanwhile, a separate study from Juniper Research estimates that the value of the embedded finance market will exceed $138 billion in 2026, up from $43 billion in 2021. McKinsey also suggests that the market could double in size within the next three to five years.

While payments will continue to be one of the biggest segments of embedded finance, embedded lending is a massive opportunity for market players. Thus, embedded finance-driven business lending is projected to grow fivefold over the next five years, from $200 million in 2021 to $1.3 billion by 2026. Meanwhile, lending embedded at the point of sale, i.e. buy now pay later services, is expected to account for just over 50% of the embedded finance market in 2026.

Although remaining a lesser revenue source, embedded insurance still holds promise to boost the uptake of insurance for high-value products with e-commerce users.

Who are the market players?

Embedded finance opportunities arise for every platform operator having frequent (often daily) digital interactions with its end customers. The types of businesses well-positioned to offer embedded finance solutions typically include retailers, business-software firms, online marketplaces, platforms, telecoms companies, and original equipment manufacturers. As the demand for embedded finance solutions grows, new players may soon enter the market as well.

To deliver an embedded finance solution to the end customer, platforms rely on a range of financial institutions that grant access to their services. Those divide into technology providers and balance sheet providers.

Some banks and fintechs fulfil both functions, providing platforms with a comprehensive suite of services.

Who gets the most market value?

Financial benefits for market players are distributed unevenly, depending on their role in embedded finance. The most significant revenue flows go to those who incur more risks and to those owning the customer relationship.

According to McKinsey research, 55% of the revenues from embedded-finance lending products go to balance sheet providers, as they bear credit default risks. Another 30% of these revenues go to distributing platforms. At the same time, distributors benefit most from payment and deposit products since they are responsible for end-customer relationships.

Meanwhile, technology providers try to capture a larger share of embedded finance revenues by increasing their share in the lending risk. Today is the best time for embarking on embedded finance for growing tech companies focused on increasing profitability while keeping acquisition costs stable.

For instance, they may offer repurchase agreements for loans originated by balance sheet providers. Tech companies are also better suited to offer creditworthiness profiles because of the rich data they can collect from their customers.

Digital-first organisations are the ones to take the best advantage of the embedded finance sector’s expansion. Their access to more sophisticated technologies, algorithms and data give them an edge in targeting the most creditworthy customers. However, as open APIs proliferate, banks can also increasingly leverage their existing user relationships and trusted brands to create compelling embedded finance propositions, especially in the BNPL sector.

Source: unsplash

Ways to succeed in embedded finance

Differentiate. To stand out among their competitors, embedded finance providers must differentiate themselves with product breadth or depth, as well as program management support.

Many distributors start offering a range of embedded finance solutions gradually. You can start with payment acceptance or deposits and then collect enough customer data to extend the product portfolio to embedded lending products.

Or else, develop deep expertise in specific embedded finance categories to cater to the niche audience. For instance, selected distributors develop innovative use cases such as just-in-time fund deposits into cards or crypto-linked payment authorisation for their end customers, understanding their specific financial needs.

Meanwhile, embedded-finance technology providers can stand out by offering sales, servicing, and risk management expertise to the new market entrants. Distributors require this kind of program management as they wish to avoid regulatory hurdles.

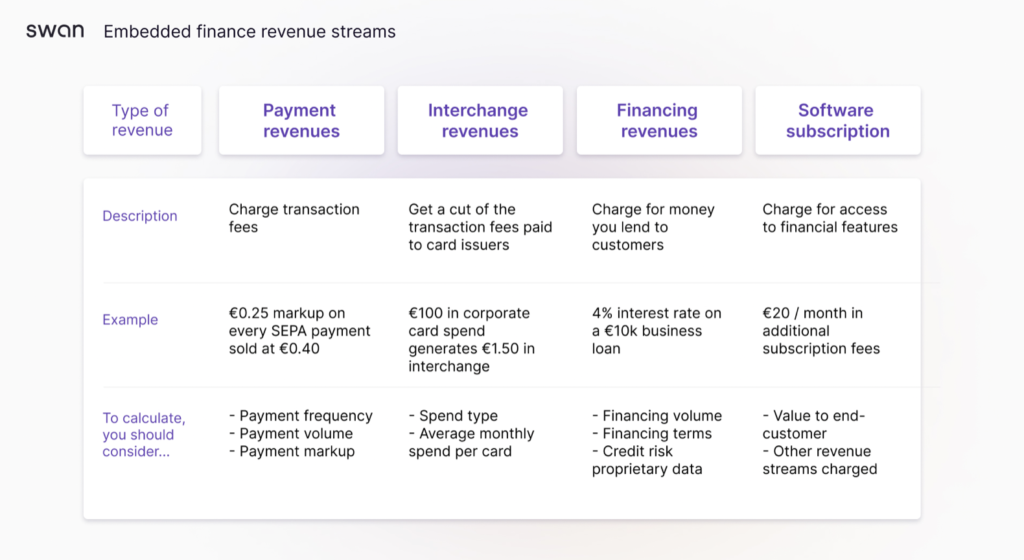

Experiment with pricing. Moreover, an embedded finance product’s success depends on a smart pricing model. Higher subscription fees aren’t the only way to monetise a product with embedded finance. Here are some suggestions from the French fintech Swan:

Source: swan.io

To receive expected revenues from the new embedded finance product, you can experiment with a range of pricing strategies:

- High-margin software + low-margin financial features

- Low-margin software + high-margin financial features

- Medium-margin software + medium-margin financial features

Combine legacy and innovative services. Traditional financial institutions with legacy technologies can use embedded finance to rethink their core business and drive growth through new services. For instance, banks with limited footprints or localised relationships, e.g. community banks and regional banks, may use embedded finance solutions to expand their revenue base through more advanced products and support.

However, to do this, banks and legacy financial services infrastructure firms must update their processes and workflows to build a modern developer experience, and provide third-party developers with self-service access and well-documented APIs.

SEE ALSO:

Goldman Sachs partners Modern Treasury to push embedded payments