Tesco Bank is a customer-orientated financial services provider

Tesco Bank: savings products and credit cards overview. Source:facebook.com

Whatever part of the world you live in, you’ve most probably heard or even shopped at one of the Tesco brand supermarkets. After all, this commercial old-timer is among the top 10 most profitable retail chains in the world. However, Tesco brand is not only about fresh groceries. The corporation has also entered the financial services market with a fully-fledged banking solution.

Tesco Bank is a customer-orientated financial services provider introduced by the British transnational corporation Tesco PLC. It offers a range of simple and convenient retail banking and insurance products including popular credit cards.

A bit of history of Tesco Bank

The bank was formed as a joint venture of The Royal Bank of Scotland and Tesco, the largest supermarket in the UK. Tesco later acquired the Royal Bank of Scotland shares. This way, the bank became a wholly-owned subsidiary. It now operates under its own banking license under the Financial Services Compensation Scheme, the UK’s deposit guarantee program.

In 2016, the bank faced the “unprecedented” hacking attack on its online accounts which resulted in a loss of around £2.5m. At the time, experts were describing the incident as the most serious attack to ever hit the United Kingdom’s banking sector.

After two years of investigation, the Financial Conduct Authority (FCA) ultimately fined Tesco Bank for “failing to exercise due skill, care and diligence in protecting” its current account holders. The fine of £16.4m was largely attributed to the fact that the bank didn’t react to the warning signs properly.

Nevertheless, Mark Steward, executive director of enforcement and market oversight at the FCA, acknowledged that:

Subsequently, Tesco Bank has strengthened its controls with the object of preventing this type of incident from being repeated.

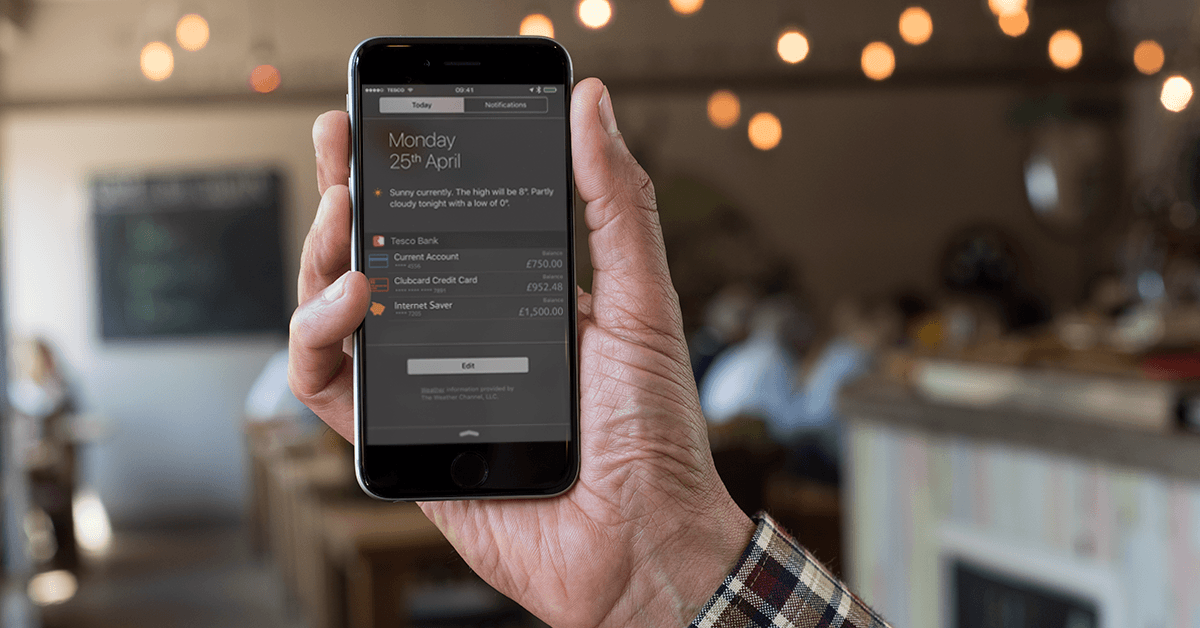

Products and services

The main segments of the bank operations include:

- Mobile banking

- Online banking

- Telephone banking

- In-store services

- Insurance

- Current accounts

- Travel money

- International transfers

- Credit cards

- Loans

- Mortgages

- Savings products

Currently, the bank has stopped opening new current accounts so only existing customers can use this service. Tesco’s current account is for personal (non-business) use only and it comes with a debit card with contactless functionality.

There’s a range of savings products offered by Tesco. Source: facebook.com

There’s a range of savings products offered by Tesco.

- Instant savings accounts are suitable for those customers who want to earn some money in a flexible way. That means topping up and withdrawing without a certain schedule. Some daily withdrawal limits apply though. Currently, the interest rate for this type of savings is 0,35% but it’s going to fall to 0,10% this August.

- Fixed-rate savings bring some certainty setting stable interest rates for the whole saving period. The interest can be received annually or monthly. Customers should make a single deposit between £2,000 and £5m within the first 30 days of account opening. That lets them earn up to 1% interest during the 1 – 5-year term.

- Tax-free cash ISA savings give you an opportunity to earn interest exempt from taxation. There are both fixed-rate and instant-access variants to save money without taxes. You can also start saving for your children’s future with the Junior Cash ISA that adds around 3% interest to your funds of up to £9,000.

Travel money is basically a currency exchange service with zero commission fees. The convenient option “Click and Collect” allows you to order your travel money online and pick it up from over 560 Tesco stores, or have it delivered directly to your home. If you prefer the old-fashioned way, you can exchange currencies instantly at over 360 in-store travel money bureaux. The unspent holiday money can be exchanged back into Pounds with the in-store buy-back service. Unfortunately, at the time of lockdown, all the in-store travel money bureaux are temporarily closed making the service unavailable.

Tesco Bank credit cards

The options delivered by Tesco Bank differ depending on the purpose of a credit application. Their representative APR is a bit lower than the average APR registered in the UK, in December 2019 (20,77%). Moreover, there’s a little cashback on purchases in the form of reward points.

When you make purchases with Tesco credit cards, you earn 1 Tesco Clubcard point for every £4 spent in Tesco and every £8 spent elsewhere. One Clubcard point is then worth 1p in Clubcard vouchers which you can either redeem in store or exchange for reward tokens.

Furthermore, you can share the benefits of your credit card by adding an additional cardholder (aged 18 or over). They’ll receive their own card and PIN allowing them to spend on your account. You’ll be responsible for all transactions and charges incurred by your additional cardholder.

Purchases card

It helps to spread the cost of your spending with the longest 0% interest period on purchases – up to 20 months. The representative APR rate and the interest rate on purchases are both 19,9% with an assumed credit limit £1,200.

For the first 3 months of use, customers also have 0% interest on balance transfers and money transfers. However, balance transfers cost 2.9%, while the money transfer fee rises to 3,94%.

You can apply for this card if:

- You have an annual income of at least £5,000 and a good credit history

- You are at least 18 years of age, live in the UK, or have a British Forces Post Office address

- You don’t currently hold more than 1 Tesco Bank Credit Card and have not applied for a Tesco Bank Credit Card in the last month

Balance transfer card

It offers the longest 0% interest period for balance transfers up to 26 months. This rate applies to any balances transferred within the first 90 days of account opening. You can transfer up to 95% of your available credit limit. The balance transfer fee is 2.98%.

Zero-interest money transfers are applicable within the first year. At the same time, the money transfer fee is 3.94%.

The representative APR rate and the interest rate on purchases are equal to those applicable for the purchases card: 19.9% with an assumed credit limit of £1,200. The eligibility criteria are also the same.

Foundation card

This one is radically different from the first two products. It is designed specifically to help people with a bad or impaired credit score to get back on track and stay in control. The card may also become a good beginning for those new to the credit concept.

It offers a no zero-interest introductory period with the interest rate higher than for other Tesco credit cards – 27.5%. Nevertheless, this rate is lower than the average APR for credit-builder cards which is 35.2%.

Still, clients with a bad credit score can enjoy some benefits:

- Monthly repayments can be as low as £25

- Starting credit limits ranging between £250 – £1,500

- The individual credit limits can be revised and are subject to increases if you manage your account well

- You can track changes in your credit score with monthly credit updates in your Tesco Bank CreditView, provided by TransUnion, as well as get an insight of the influence of your specific spending habits on your overall credit score

The conditions of the application are similar to those mentioned above for other credit cards with the exception of the good credit history requirement.

Drawbacks of Tesco Bank

Drawbacks of Tesco Bank. Source: facebook.com

Although the products themselves stay competitive and have fair rates, when it comes to putting customers first, Tesco Bank fails to comply.

It seems that this bank doesn’t have very nice customer service. In fact, the reviews on TrustPilot label Tesco Bank services as bad (1.4 out of 5). Only 9% of respondents believe this financial institution shows an excellent performance, while a staggering 83% have graded it with the lowest score.

The common issues mentioned include unhelpful and impolite operators, inability to reach customer support, long term of handling dispute resolutions and refunds, as well as many more problems with insurance products.

Moreover, in the challenging times of COVID-19 pandemic, the bank has provided its customers with a negative experience.

Despite the promises that credit holidays offered by most lenders in the UK won’t affect individual credit scores, many Tesco Bank clients were unpleasantly surprised to find out their default on payments was registered by the credit agencies.

Due to the severe impact of the Coronavirus crisis on the national economy, a few months of overdue debt is not generally going to count as the personal inability to manage finances.

However, many Tesco Bank clients were warned to the contrary and brought it out to the media. The bank confirmed that there have been a few cases

where a missed payment had been registered [with credit agencies] before the payment break has been processed.

They promised to fix the issue, but the event added up to customer frustration caused by Tesco banking services.

SEE ALSO: