Blockchain’s impact transcends cryptocurrencies, offering transformative potential across diverse industries due to its decentralized and cross-border nature. However, legal and regulatory considerations warrant attention to maximize its benefits. Its magic potion? Decentralization. With no central authority dictating the flow, blockchain empowers seamless cross-border transactions, shaking the very foundations of the financial landscape.

Let’s discover the challenges and opportunities that blockchain presents, and chart the evolving regulatory landscape navigating this uncharted territory.

The Key to Unlocking a New Era of Innovation

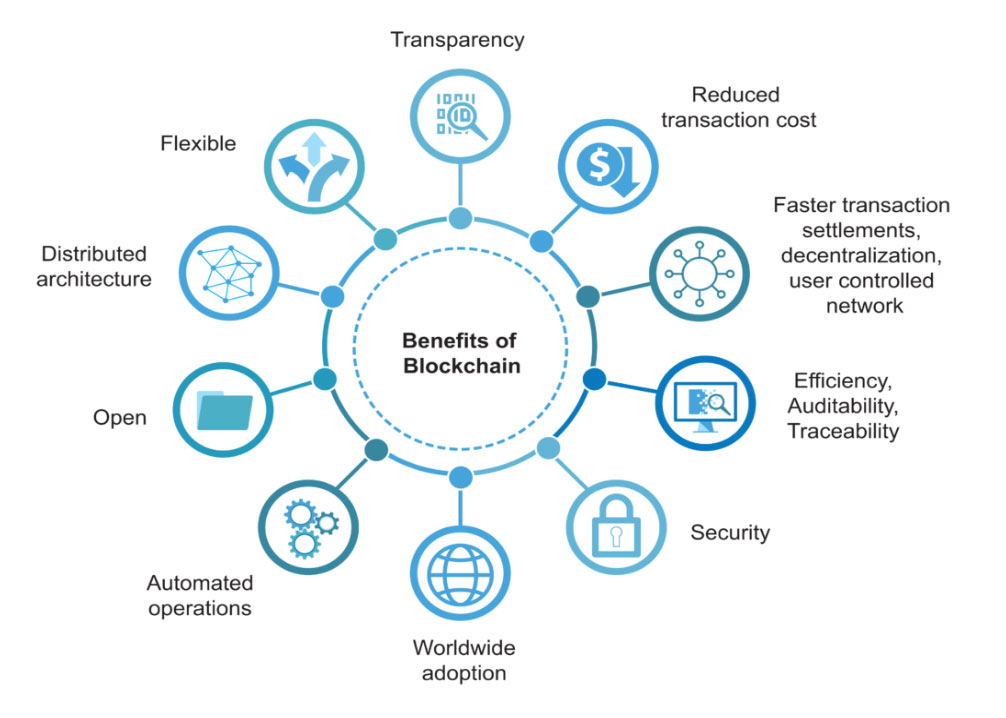

While its decentralized nature and cross-border applications pose unique challenges, these same features also hold immense potential to transform legal processes, enhance security, and foster transparency.

Enhanced Transparency and Traceability

Blockchain’s transparency and immutability provide a groundbreaking solution to enhance transparency and traceability in various sectors, from supply chains to financial markets. Imagine a world where every step of a product’s journey, from raw material extraction to final delivery, is meticulously recorded and accessible to all stakeholders. Blockchain enables this exact scenario, creating a transparent and verifiable trail that eliminates the possibility of manipulation or fraud.

This newfound transparency holds immense promise for industries grappling with issues like counterfeit goods, supply chain disruptions, and financial fraud. For instance, in the pharmaceutical industry, blockchain can ensure the authenticity of drugs by tracking their movement from manufacturing facilities to pharmacies. In the financial markets, blockchain can prevent illicit activities by providing an immutable record of transactions.

Enhanced Security

Blockchain’s tamper-proof nature is another transformative feature that can revolutionize the legal and regulatory landscape. Think of sensitive data, such as personal information or intellectual property, as precious jewels. Blockchain acts as an impenetrable fortress, safeguarding these jewels from unauthorized access, modification, or deletion.

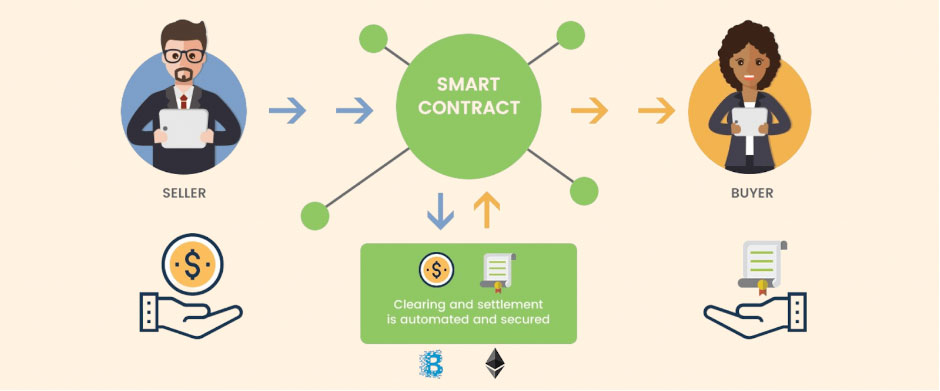

This enhanced security is particularly crucial in the legal world, where sensitive client data and confidential transactions are paramount. Blockchain can securely store and manage this data, protecting it from cyber threats and ensuring data integrity. Additionally, blockchain can power smart contracts, self-executing digital contracts that eliminate the need for intermediaries, further enhancing security and reducing the risk of fraud.

Efficiency and Automation

Blockchain’s efficiency-enhancing capabilities are a game-changer for legal and regulatory processes, often plagued by manual labor, lengthy paperwork, and communication bottlenecks. Blockchain can streamline these processes, automating tasks, and reducing the risk of human error. Manual paperwork, slow-moving approvals, and international barriers – blockchain tackles these hurdles head-on, revolutionizing how we manage legal and regulatory activities.

The Regulatory Maze: The Decentralized Nature of Blockchain

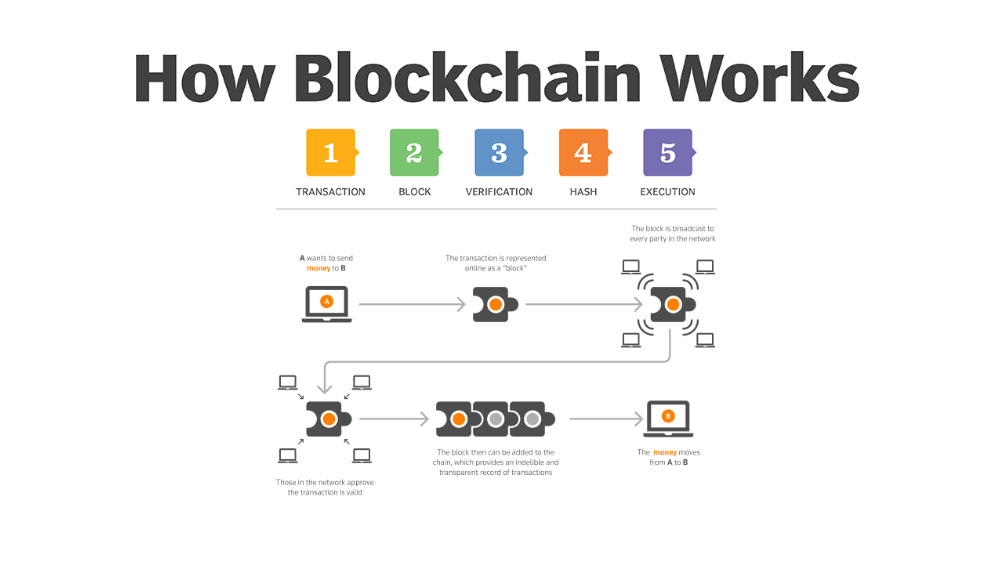

Blockchain, the brainchild of Satoshi Nakamoto, has revolutionized the way we perceive and interact with digital information. Its decentralized architecture, while a cornerstone of blockchain’s security and transparency, also throws a wrench into the gears of traditional regulatory frameworks. Picture a traffic warden accustomed to directing the flow of cars at a single, well-defined intersection. Now, unleash them into the bustling square – with its myriad pathways, impromptu stalls, and ever-shifting pedestrian routes. The task of enforcing rules and ensuring order becomes infinitely more complex.

The Regulatory Paradox of Decentralization

The burgeoning world of blockchain technology faces a critical crossroads – the paradox of decentralization. As a system built on distributed databases and peer-to-peer networks, blockchain unlocks a treasure trove of opportunities. It promises to democratize finance, slashing transaction costs and opening doors to financial inclusion for underserved communities. Imagine a world where cross-border payments are frictionless, financial services are accessible to all, and innovation flourishes without the shackles of centralized intermediaries.

Jurisdictional Boundaries: A Transnational Challenge

Unlike traditional financial transactions confined within national borders, blockchain transactions dance across continents, weaving through a labyrinthine web of jurisdictions. This borderless nature creates a regulatory Rubik’s Cube, where establishing clear authority becomes a game of untangling the intricate threads of international law.

Imagine a scenario where two individuals, Alice in Paris and Bob in Tokyo, engage in a cryptocurrency transaction. Their digital handshake isn’t just a point-to-point connection; it ripples through a network of validating nodes scattered across the globe. This distributed ledger, the lifeblood of blockchain, becomes a jurisdictional puzzle. Should French or Japanese laws govern the transaction? What about the nodes located in Singapore or Brazil? This lack of a single governing authority opens a Pandora’s box of legal complexities.

AML/CFT: Tackling Money Laundering and Terrorist Financing

Criminals can effortlessly transfer illegal funds across borders, exploiting the lack of central oversight and traditional AML/CFT controls. But regulators walk a tightrope between fostering innovation and safeguarding the financial system. Implementing traditional AML/CFT measures in a decentralized world proves highly complex. Identifying suspicious transactions amidst a sea of anonymous addresses and tracing the ultimate beneficiary of funds becomes a daunting task.

Fortunately, the fight against blockchain-enabled crime isn’t one-sided. A burgeoning ecosystem of startups and established players is developing innovative solutions. These include:

- Transaction monitoring tools: By analyzing patterns and identifying anomalies in blockchain activity, these tools can flag suspicious transactions for further investigation.

- KYC/AML compliance platforms: These platforms help blockchain-based businesses implement KYC (Know Your Customer) and AML (Anti-Money Laundering) measures, even in a decentralized environment.

- Public-private partnerships: Collaboration between governments, blockchain companies, and financial institutions is crucial for developing effective and coordinated responses to illicit activity.

Strengthening the Regulatory Framework

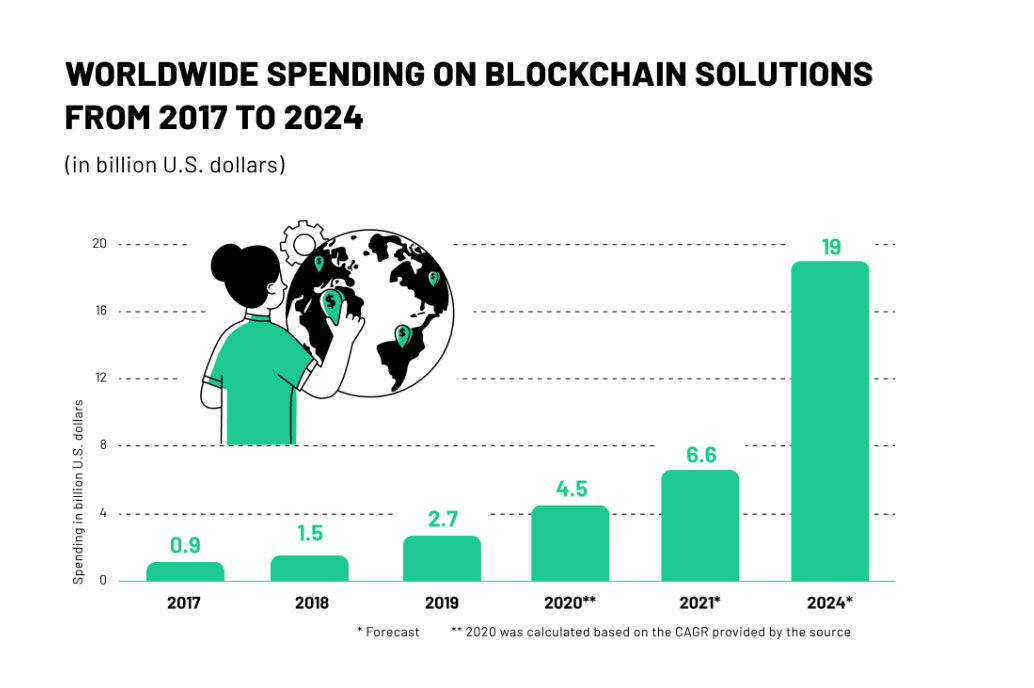

The burgeoning world of blockchain technology is brimming with potential, promising to revolutionize everything from finance and supply chains to healthcare and voting. However, one major hurdle impedes its widespread adoption: the lack of clear and consistent regulatory frameworks.

This regulatory fog has several detrimental consequences:

- Uncertainty for businesses: Companies developing or implementing blockchain solutions are often left guessing about the legal and compliance implications. This hesitation can stifle innovation and hinder investment.

- Investor apprehension: Without clear rules of the road, potential investors may be wary of pouring their money into blockchain projects, fearing regulatory backlash or unforeseen legal complications.

- Market fragmentation: Different jurisdictions adopting diverging regulatory approaches can create a patchwork of rules, hindering the seamless flow of blockchain-powered applications and services across borders.

So, what’s the way forward? While a one-size-fits-all global regulatory framework might not be feasible, there are steps that can be taken to mitigate the uncertainty and pave the way for responsible blockchain adoption.

International Cooperation: Bridging the Global Divide

To address these challenges, regulators are increasingly turning to international cooperation as a means of establishing consistent and effective oversight. By fostering collaboration among regulatory bodies across different jurisdictions, they can develop harmonized frameworks that provide clarity and predictability for businesses operating in multiple markets.

This approach is evident in the establishment of the Financial Action Task Force (FATF), an international body that sets standards for combating money laundering and terrorism financing. The FATF’s recent guidance on virtual assets, while not binding, provides a valuable framework for regulators worldwide to address the risks associated with blockchain technology.

Regulatory Sandboxes: Testing the Waters of Innovation

Regulatory sandboxes offer another innovative approach to adapting to the challenges posed by blockchain. These experimentation zones provide a safe environment for blockchain-based projects to operate under a flexible regulatory regime, allowing regulators to gain insights and adapt their policies in real-time.

The UK’s Financial Conduct Authority (FCA) has been a pioneer in the use of regulatory sandboxes, granting licenses to a number of blockchain-based companies to operate in a test environment. This approach has allowed the FCA to gain valuable experience in regulating this new technology and to identify potential risks and opportunities.

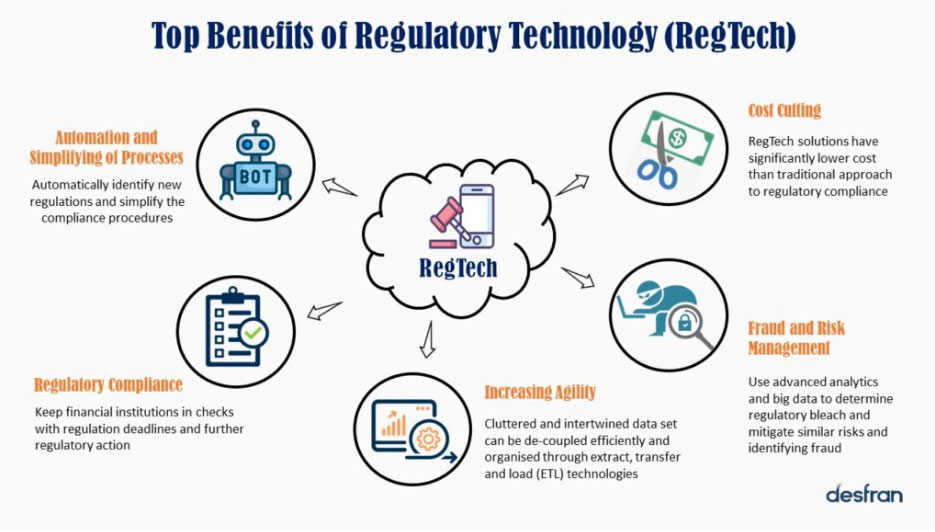

Regulatory Technology (RegTech): Leveraging Technology for Compliance

Regulatory technology (RegTech) is rapidly emerging as a powerful tool for regulators to address the challenges of blockchain. RegTech solutions can automate compliance checks, monitor blockchain activity for suspicious behavior, and provide real-time insights to regulators.

For example, blockchain analytics companies can track the movement of funds and identify potential illicit activity, while RegTech platforms can automate the process of verifying customer identities and conducting due diligence checks. These tools can help regulators to effectively oversee the growing blockchain ecosystem and mitigate risks.

Challenges and Concerns

The Scalability Conundrum

Imagine a bustling highway where only a few cars can pass at a time. That’s essentially the dilemma faced by blockchain networks, particularly those based on the original Bitcoin protocol. With increasing adoption and transaction volumes, the network can get congested, leading to delays and higher transaction fees.

To address this challenge, researchers have proposed various solutions, including sharding, which divides the network into smaller, more manageable shards, and layer-2 solutions, which add additional layers of processing to the network. These solutions have shown promise in improving throughput, but they come with their own complexities and trade-offs.

Energy Consumption: A Cost-Benefit Analysis

Blockchain’s energy consumption has sparked debate, with some criticizing it as wasteful and environmentally harmful. The primary culprit is blockchain mining, the process of validating transactions and adding new blocks to the blockchain. This process often involves competing miners using powerful computers to solve complex mathematical puzzles, requiring substantial energy input.

While energy consumption is a valid concern, it’s essential to consider the benefits that blockchain brings. For instance, cryptocurrencies like Bitcoin provide a secure, decentralized alternative to traditional financial systems, which often rely on centralized institutions that consume energy in their own right. Additionally, blockchain-based applications, such as smart contracts, can automate transactions and reduce bureaucratic inefficiencies, potentially leading to overall energy savings.

The Adoption Curve: Gaining Traction

Blockchain technology is still relatively young, and its adoption rate among businesses and individuals has been slow. This is due to various factors, including the complexity of the technology, concerns about security and regulation, and a lack of clear use cases.

However, there are signs of progress. Several multinational corporations are exploring blockchain applications, and governments are increasingly experimenting with blockchain-based solutions. As adoption grows and use cases become more evident, blockchain is likely to gain wider acceptance.

Real-World Blockchain Success Stories

Tracking Your Tuna from Ocean to Plate

Remember all that talk about revolutionizing supply chains? Well, guess what? It’s actually happening. Companies like IBM and Walmart are using blockchain to track food from farm to fork, ensuring transparency and safety. Imagine knowing exactly where your tuna came from, and being able to verify its freshness with a few clicks. No more mystery meat!

Ending the Blood Diamond Trade

The diamond industry has long been plagued by ethical concerns. But blockchain is changing the game. Platforms like Everledger are using blockchain to track diamonds from mine to market, ensuring they’re not conflict diamonds. So, you can finally sparkle with peace of mind, knowing your bling isn’t finding any nasty wars.

Democratizing the Art World with NFTs

NFTs, or non-fungible tokens, have taken the art world by storm. These digital certificates of ownership allow artists to sell their work directly to collectors, cutting out the middleman and democratizing the art market. Beeple’s $69 million NFT sale may have been headline-grabbing, but even smaller artists are finding success with NFTs, building communities and monetizing their work in new ways.

Fair Pay for Musicians in the Streaming Age

The music industry has been struggling for years, with streaming services squeezing out artists. But blockchain is offering a glimmer of hope. Platforms like Audius are using blockchain to ensure musicians get paid fairly for their streams, cutting out the exploitative middlemen and giving artists a chance to actually make a living from their music.

Conclusion

The blockchain buzz is real, and it’s not just about crypto bros and cat memes anymore. This technology is quietly weaving its way into everything from supply chains to healthcare, promising transparency, security, and a whole lotta efficiency.

Imagine your business, humming away like a perfectly oiled machine, powered by blockchain magic. Choosing the right custom blockchain development company is an investment in your future. With the right partner by your side, you can unlock the transformative potential of this technology and revolutionize your industry. Remember, it’s not about finding the biggest, flashiest name, but the team that gets you, your vision.