Daniel Martin

Author

It is so exciting and fulfilling to bring a world-class innovative solution that addresses a real existing problem. A recent example is the pharmaceutical companies’ innovative drive to contain the coronavirus during the pandemic with vaccines in the shortest possible time.

BioNTech and Moderna – considered biotech startups, leveled up vaccine production to complement big pharma. We can’t picture what the world would be like without their timely intervention.

However, it took a pandemic to realize these biotech startups’ success stories.

Unfortunately, several startups still fail. Continuous innovation is necessary to uncover new business opportunities and stay in a highly competitive business environment.

Source: Flickr

But the high uncertainty levels make innovation a risky affair. This may cause some firms to ignore taking essential risks. And even if they do, they may develop the wrong solution using flawed data or assumptions.

And that’s the exact situation that worried Eric Ries, author of Lean Startup, too. He stated, “What if we found ourselves building something that nobody wanted?”

Whether you deliver the innovative solution on time or a budget does not matter. If nobody wants it, it won’t go anywhere. That’s a recipe for failure. And it’s affecting many startups.

According to CB Insights, lack of market need is the second leading reason for startup failures after lack of capital. It accounts for 35% of failures.

But, startup failure is a complex problem in the innovation space that goes beyond market need. The Lean Startup innovation accounting can easily handle its complexity.

What Is a Lean Startup?

Source: Wikimedia Commons

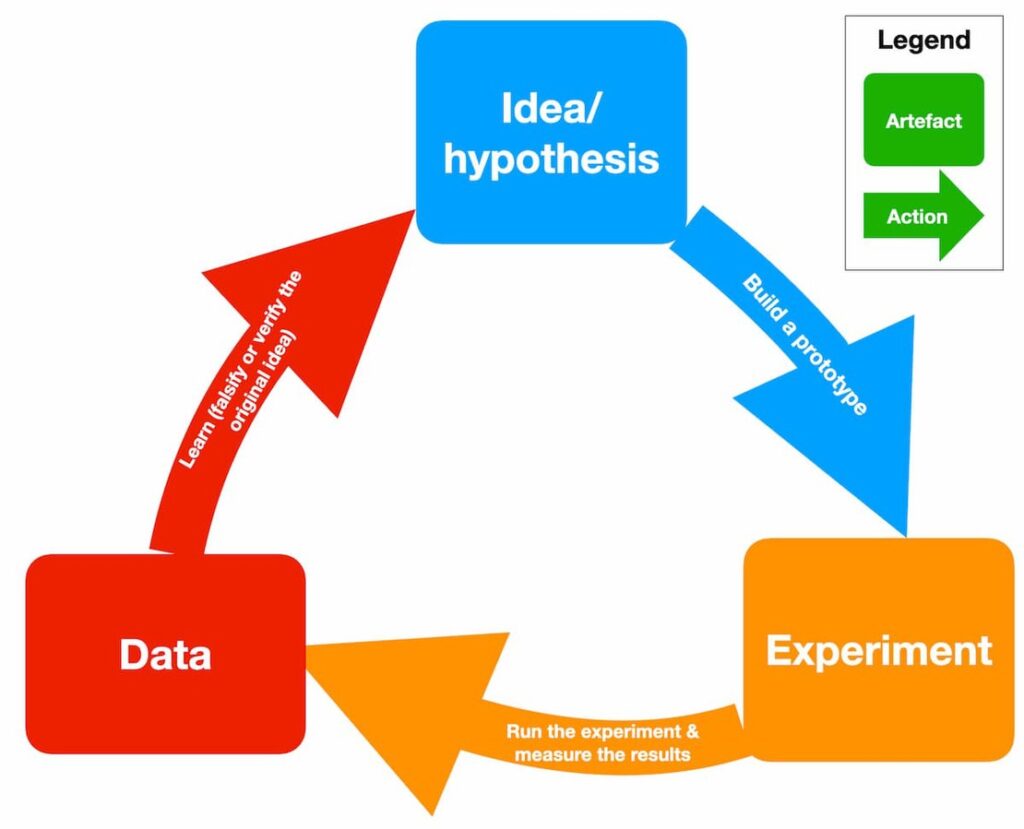

It’s a revolutionary approach to the continuous innovation process. It helps shorten product development time and test the viability of the proposed business model or product.

The approach achieves this through experimentation, validated learning, and iterative product releases based on customer feedback. The best and most important aspect of the Lean Startup approach is that it gives you the needed framework to evaluate and measure your innovation progress.

At the core of this framework is innovation accounting (IA). Innovation accounting complements your traditional accounting in tracking your innovative products. Traditional accounting heavily rely on metrics like market share, return on investment (ROI), and profit and loss statements.

These traditional accounting metrics are suited for mature products with historical records to base calculations and references. You don’t have that luxury when dealing with innovation projects. They are new projects with no past data and in an uncertain environment.

Plus, the early stages of innovation projects are too fluid to gauge their viability and profitability. You may not wish to throw the baby with the bathwater. But that can happen in innovation projects – particularly if they are tied to a less-equipped and rigid traditional accounting approach.

Enters the suitable solution – innovation accounting.

What Is Innovation Accounting?

Innovation accounting is a structured approach to measuring innovation progress and success. It is one of the core principles of the Lean Startup approach. Other principles include:

- Entrepreneurs are everywhere

- Entrepreneurship is management

- Validated learning

- Build-Measure-Learn

The crucial factor in a startup is understanding and learning about the innovative project(s).

Since it is flexible to a startup’s early stage fluidity, innovation accounting for startups is suited to measure your new projects’ progress. Basically, innovation accounting works best for startups that when the corporate metrics, used to measure business success, are still at 0.

It allows you to develop relevant metrics that provide insights into your projects. Most of the insights are geared towards:

- User engagement. It investigates customer needs to make the product customer-centric.

- Product-market fit. It helps gauge and establish market need. That can eliminate the second leading cause of startup failures, as highlighted at the beginning of the article.

- Scalability. Helps launch the product on the broad market after establishing its product-market fit. Loosely put, it drives the product towards financial performance at this stage.

In short, innovation accounting for startups is a vital ingredient for product development and scaling. But how does innovation accounting help guide and scale your innovative projects?

How Lean Startup Innovation Accounting Works

Innovation accounting revolves around three levels for accurate and better metrics and insights for the build-measure-learn cycle.

- Customer’s needs and feedback. It involves tracking aspects like user discussions, conversion rates, and feedback. It allows you to gauge user involvement in product development. It will also help test your business hypothesis through a minimum viable product (MVP).

- Testing the product’s assumptions. It handles assumptions around the values new users will gain from your new product. Also, it addresses notions around market growth due to new customers that will use the products.

The second-level insights are drawn from the prototyping, MVP, and validated learning. All these further guides your product development. Some metrics to check out for user value testing include repeat purchases and retention rates.

For growth assumption evaluation, the suitable metrics may include referrals or the ability to reinvest one customer’s revenue to acquire another. At this level, the MVP is tested and iterated many times with users’ input. So, it helps move the project from baseline to almost a real ideal product. - Real present value of the product. It presents the net present value of the product. The third level will help indicate the current worth of your product. It will have solid traction to decide whether to continue (persevere) or change to a new strategy (pivot).

If the indicator shows that you should pivot, then you’ll need to start over again in a more impactful and productive design than before. Some metrics applicable at this level include trial volume, trials converted into customers, or average pay from users.

In short, the last level defines the product’s financial performance.

The three levels capture the dynamic nature of the cycle of continuous improvement. So, lean startup innovation accounting is not static. It changes with every single iteration and change that is made. That also comes with new data to gauge whether you are making improvements or not.

So, it gives a clear path of the product’s development from idea to the market.

Source: Wikimedia Commons

So, you can apply the lean startup innovation accounting in three simple steps:

- Set the metrics suitable to your project. For example, you should investigate whether you did what you promised to do or if there are improvements for users.

- Run the metrics on the IA’s three levels discussed above. Collect the data and evaluate progress.

- Hold the innovative project accountable. Check whether it is geared towards customers’ needs. So, it should show progress and the direction it is taking.

Final Takeaway

Innovation accounting simplifies how you measure and track your innovative projects without losing sight of the crucial details. Your experimentation, iterative developments, and validated learning are all woven together by innovation accounting.

So, collectively all chained indicators can be tracked to evaluate your innovation’s progress. We’ve discussed how you can get started on this important aspect of the lean startup approach.

But it is understandable if setting your metrics and running them on the three IA levels is overwhelming. You may need to engage with innovation accounting professionals for guidance in such a case.

SEE ALSO:

8 Ways to Protect Your Identity From Theft