![]()

Bader Al Hussain

PaySpace Magazine Analyst

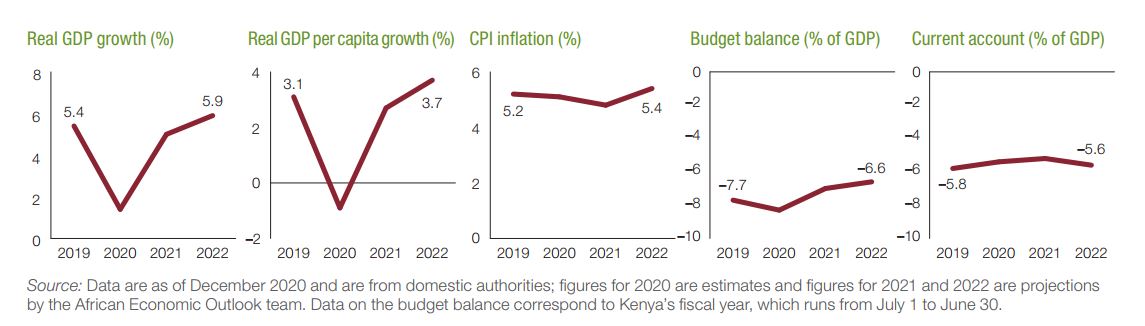

Similar to the majority of the countries, Kenya also experienced the devastating effects of the COVID-19 pandemic on all spheres of life. On the economic front, the country’s GDP growth decelerated to 1.4 % in 2020 as compared to 5.4% in 2019. The primary drivers of the growth came from agriculture as it was the least affected sector during the pandemic. The government introduced expansionary fiscal policies in order to mitigate the adverse financial impacts of the lockdowns, especially to the impoverished segments of society. Concomitantly, the central bank also slashed the interest rates in order to further stimulate the economy.

According to the estimate given by the African Development Bank Group, owing to the pandemic, approximately 900,000 Kenyans lost their jobs, resulting in nearly 2 million people pushed into poverty.

Kenya’s economic forecast 2021: what’s coming next? Source: pixabay.com

Economy at glance

Kenya is a market-based economy with a nominal GDP of approximately USD 106 billion and is considered as the third largest economy in Sub-Saharan Africa, coming behind Nigeria and South Africa. According to the World Bank’s ease of doing business index, the country is ranked 56th in the world. With the GDP per capita of $2,129, the country is largely classified as a lower-middle income country. The major industries of the economy are agriculture, forestry, fishing, mining, manufacturing, energy, tourism, and financial services.

As far as the structural composition of its economy is concerned, the country’s agriculture contributes 34.5% to the whole national output whereas industry and services account for 17.8% and 47.5% respectively. On the stability of the economy, Standard and Poor furnished the credit rating of “B+” with a stable outlook. Additionally, the country’s foreign reserves are hovering at approximately USD 8 billion, providing an import cover of nearly 6 months.

Kenya economy outlook

Historically, the Kenyan economy has been growing at an average rate of 4.78% per annum since 1961. The prospective growth of the country is largely contingent on the number of reforms the government undertakes in order to increase its productivity. According to the World Bank report, the country has made significant reforms in order to foster its economic growth, social development, and political stability over the past ten years. These reforms underwent a kickstart when the new constitution was passed in 2010 that introduced a bicameral legislative house, devolved county government, a constitutionally tenured judiciary and electoral body.

The outlook for the Kenyan economy is positive, whereby GDP growth is expected to grow at 5.0% and 5.9% for 2021 and 2022 respectively. The graphs below illustrate the historical and prospective key economic matrices of Kenya.

Going forward, with a sharp rise in commodity prices all over the world, the country is expected to experience a rise in the inflation rate, especially food inflation. However, the impact of inflation can be offset by an expected rise in their income levels in the post-pandemic phase. Further, the unprecedented rebound in the global economy has created a supply-side disruption that has created transient supply shocks together with rising commodity prices. These issues are expected to have an adverse impact on the current account position of the country as it is expected to import more goods and services amidst rising economic growth.

Kenya stock market performance

The Nairobi Securities Exchange is the primary stock exchange of Kenya based in Nairobi. NSE All-Share Index tracks the performance of all stocks listed on the Nairobi Securities Exchange. The Nairobi Securities Exchange share index fell 20% between 30 September 2019 and September 2020, and market capitalisation fell 2% over the same period. However, the market recovered owing to the unprecedented rebound in the economy.

NSE All-Share Index gave a 1-year return of almost 21.69 per cent and the year-to-date (YTD) return of 11.68 per cent. Thus, an index is currently trading at a P/E multiple of 14.34x and P/B multiple of 1.67x. Going forward, in order to make its capital markets more vibrant and robust, Kenya needs to increase its market capitalisation to GDP ratio by incentivising more entities to list their shares on the stock exchange. Further, Nairobi Securities Exchange can introduce more reforms in order to increase the transparency, leading to a greater depth (i.e., more local and international investor participation) in its capital markets.

Progress towards a middle-income country

The government has drafted a long-term development plan by the name of “Vision 2030” and this plan aims to transform Kenya into a middle-income country into a comity of nations by the year 2030. The reforms and initiatives required to attain this milestone have already been pursued. Since 2008, the government has pushed economic growth and social development through political, structural, and economic reforms. In 2017, it launched the Big Four agenda focused on food security, affordable housing, manufacturing, and universal healthcare.

Apart from the above-mentioned points, the country is poised to reap the advantages through the participation in regional and global trade opportunities through participating in the platforms such as the African Continental Free Trade Area (AfCFTA) and the African Growth and Opportunity Act (AGOA). Such initiatives are expected to boost the country’s economic productivity and accelerate Kenya’s integration into the global economy through international trade.

There are other promising indicators of progress in the country’s economy. During the first 10 months of 2019, the country attracted 54 projects with a total outlay of $2.9 billion in announced investments, according to fDi Markets, a Financial Times data service that tracks greenfield cross-border investment. This growth reflects a general rise across Africa in foreign direct investment that supports new greenfield projects. Such projects assist the country in the betterment of its existing commercial infrastructure that the country cannot fully commit to owing to its meager resources.

According to the private sector diagnostic analysis, the sectors that are expected to outperform and where there are greater opportunities of return over the next three to five years are: agribusiness, affordable housing, and manufacturing.

Conclusion

To conclude, the country is well on its way to benefit from its reform’s agenda apart from the rise in the regional foreign-funded projects. Further, acceleration in the implementation of reforms, consistency of policies, and stability of the internal and geo-political situation are the key determinants to the future of the economic landscape of the country.

SEE ALSO: