![]()

Bader Al Hussain

PaySpace Magazine Analyst

Is the current stock market expensive? Source: shutterstock.com

Introduction

The year 2020 was a time of uncertainty for the stock market. The global market initially tanked when COVID-19 cases began springing up in all parts of the world. Then the performance of technology stocks supported the stock market to some extent. However, large stimulus packages by governments coupled with the drastic cut in policy rates by central banks played a pivotal role in the rise of global stock markets as the reduction in interest rates increased the valuations of the equity investments remarkably.

Now in 2021, amid hope and excitement that the pandemic might soon be behind us due to successful vaccination campaigns, investors may find it harder to produce the kind of stock market returns we saw last year during COVID-19. Strange I know, but as we witnessed last year, equity returns did not align with the current state of the economy. Instead, stocks this year may resemble their performance in 2010, i.e., year two of the bull market that started in 2009. After the S&P 500 Index’s stunning 68% return from the March 2020 low to the end of the year, stocks are expected to take a breather, much as they did in the second quarter of 2010. Importantly, however, overall returns of the second year of a bull market are historically positive, like in 2010.

Although past performances do guarantee a future return, an intelligent investor needs to have a keen observation of historical market movements and the factors underlying those movements. Thus, the global stock market is expected to perform on the back of multiple factors. These factors can be detailed as follows:

Earnings of companies

The advent of the COVID-19 pandemic resulted in structural changes in the global economy, whereby the share of technology and IT service sectors has increased substantially. The earnings of businesses operating in these sectors increased manifold, thus attracting a huge amount of investment into their equities. Nevertheless, the technology sector has recently hit correction territory as coronavirus takes a toll.

However, the travel, hospitality, and tourism sectors took the most hits as almost all their earnings were evaporated owing to lockdowns by various governments on the back of the COVID-19 pandemic. Now as the vaccine campaign has rolled out successfully in almost all major parts of the world, the value of these businesses is contingent on their ability to recoup most of their lost earnings.

In 2021, we believe that value stocks are still cheaper relative to their historical levels. In our current economic recovery, we should see opportunities in value stocks, focusing on those companies with strong balance sheets with lower leverage ratios.

Outside of the U.S., we should see attractive investment opportunities in technology stocks of Asia (excluding Japan). This group historically benefits from U.S. dollar depreciation and technology stocks in this part of the world are trading at a steep discount to their U.S. peers.

Concerns for inflation remain

The substantial rise in commodity prices coupled with cash-rich books of households is expected to result in a higher inflation rate for the United States economy. As the Federal Reserve has shown its intention for an inflation target to be 2% per annum. The concerns for inflation can be vindicated through a steepening of the yield curve of United States treasuries. The continuous rise in yields of 10-year bonds is a developing case study.

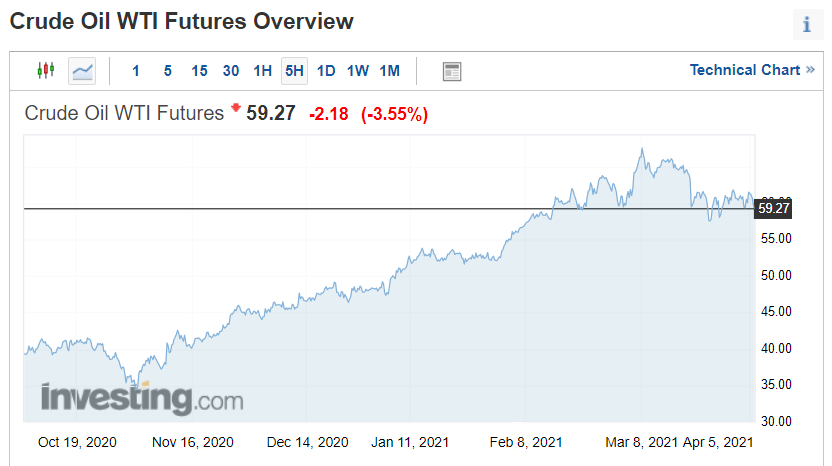

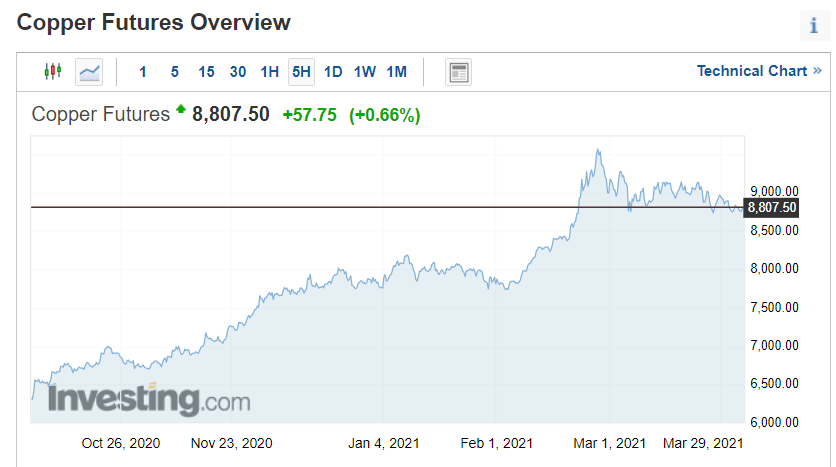

On the other hand, the sudden upsurge in global business activity has put pressure on the prices of raw materials and energy products, resulting in a spike in the prices of these commodities. For instance, the prices of oil and copper increased by 89.09% and 81.91% within a year.

Source: investing.com

Source: investing.com

Supply chain constraints

The demand for semiconductor chips rose sharply on the back of explosive demand for technology products during the pandemic. This resulted in a spike in demand for semiconductor products. Although the hike in demand from technology products was largely compensated by a drop in demand from other electrical appliances and machines such as automobiles, the unprecedented rebound in the global economy changed the whole scenario.

Variables to consider in the stock market forecast

We consider the following variables in the forecast of the stock market in 2021:

1. Multiples in the stock market

After the pandemic, there was a re-rating in the multiples of different sectors. The technology sector garnered the highest multiples, whereas cyclical stocks traded at relatively lower multiples. Now as earnings announcements start to pour in, the market will then decide whether the multiples given to these stocks are justified or not.

2. Earnings

Upcoming earnings will indicate whether companies have successfully recouped the major portion of their lost earnings or not. Given the current situation, a major rebound is expected in the travel, hospitality, and tourism industries. However, technology stocks will maintain and retain their importance in the digital world.

Is the current market expensive?

Following the strong and longest bullish spell in the stock market. Some investors are jittery, as to them, the market is overvalued, thus deterring them from investing in the stock market. Additionally, given the historically high S&P 500 price-to-earnings ratio (its market value per share divided by its earnings per share), except for the 1990s tech bubble, over the past 44 years, the market has never sustained a high price-to-earnings ratio. This adds credence to the point of view that views the market as overvalued.

However, there is a perspective that completely rejects the above-mentioned narrative. It states that if we compare the earnings yield to the US 10-year treasury, then we can safely conclude that the market is actually on the cheaper side of the equation. In addition to that, the fundamental characteristics of technology companies (such as Google and Amazon) is vastly different from that of a traditional listed company such as General Electric and Walmart.

Technology companies have a unique ability to scale and sell their products globally, with less or no restrictions all over the world. Their ability to scale their operations can massively reduce their costs for producing those products. This is because we are witnessing a huge operating margin of these technology companies, and thus, they warrant high valuations in the stock market.

Conclusion

To conclude, we see both arguments playing out to some extent. With compelling opportunities in the stock market and the potential for a solid return, this would be consistent with the second year of a bull market in equities. However, we do expect substantially higher volatility along the way. Potential market headwinds include the possibility of the Federal Reserve beginning to adjust its timeline for ultra-accommodative policies. If this happens, then the bar for companies beating earnings estimates will become less likely. Geopolitical headlines and the cash that entered the market in late 2020 will easily shake loose in 2021.

In our view, this is going to be a great year for equities. Therefore, invest in stocks whose business model is not poised for disruption in the foreseeable future.

SEE ALSO: