What do we know about PIX?

PIX e-payment system explained. Source: shutterstock.com

The new instant payment system from the Central Bank of Brazil aims to revolutionize the Latin American payment landscape.

About a year ago, Brazilian Central Bank introduced a new payment method for local population. It grew enormously popular, offering instant direct bank transfers supported by both traditional financial institutions and innovative fintechs.

PIX is the smartphone-based, instant payments technology developed and served by the main national banking institution. With PIX, transactions occur in less than 10 seconds, 24/7 – including weekends and holidays.

How it works

Users download an app and tie it to a bank account or a digital wallet. To make payments faster and not insert all the personal information manually, they also need to register an address key directly with their financial and payment institutions.

The address key bears identification of the user’s account. There are four types of address keys:

- CPF/CNPJ (taxpayer identification number)

- Email address

- Cell Phone number

- Random key – a set of random numbers, letters, and symbols

Receiving payments with PIX is possible by informing the payee of your address key, or generating a QR Code. Unlike traditional payment methods in Brazil (TEDs or DOCs), users shouldn’t manually insert the receiver’s account information. Nevertheless, the manual fill-in option is still valid if users wish to choose it.

PIX transactions are instant, meaning they are processed in real time, 24 hours a day, 365 days a year, and the funds are made available immediately for use by the recipient. These electronic payments are credited from one bank to another with the supervision of Banco Central do Brasil (BCB).

BCB is also responsible for the management and operation of PIX operational platforms:

- the real-time gross settlement (RTGS) infrastructure (SPI, “Instant Payment System”) that settles transactions between different institutions in few seconds,

- and the alias database (DICT, “Transaction Accounts Identifier Directory”) that links aliases and users’ account information.

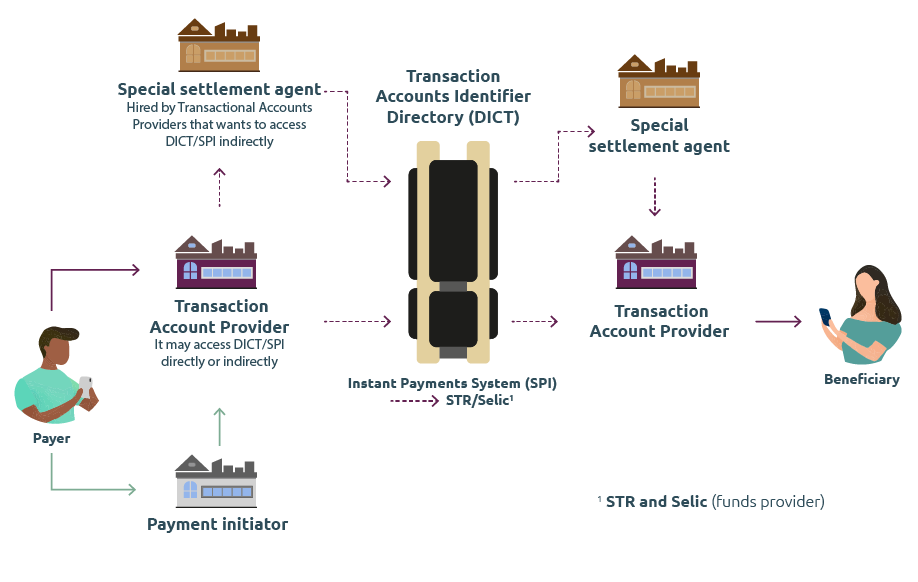

The main participants of the PIX payment scheme are:

- Transaction account provider – a financial or payment institution that provides demand, saving or prepaid payment accounts to end users.

- Special settlement agent – a financial or payment institution that participates in PIX exclusively to provide settlement services to other participants (it does not provide payment services to end users). Such an agent must be a direct participant of SPI.

- Payment initiator – a payment institution regulated by BCB that will carry out payment initiation at the request of a customer who is a transactional account holder in a financial institution or any other institution licensed by BCB. The institution does not participate in the financial settlement.

- BCB – regulator and manager of the PIX system.

That’s how all the participants interact:

Source: BCB

PIX’s operational framework has a close connection to the implementation of the Open Banking System in Brazil. This October, the country entered Phase 3 of its open banking plan. The goal of this Phase is to usher in the regulation of payment initiation from any online platform. It will enable consumers to pay for products and services using PIX, without having to use their bank’s app.

Advantages and disadvantages

PIX quickly gained popularity in Brazil and global retailers/service providers started adding this instant payment system to their checkout solutions. It’s already been used at least once by 110 million Brazilians (51% of the total population) and about $89 billion has moved through the network.

What makes the payment system so popular?

- It’s fast. Standard transaction time is 2,5 seconds, slower ones take up to 10 seconds.

- It’s ubiquitous. Pix works through multiple bank apps and different digital wallet services. All financial and payment institutions, including fintech companies, can offer their clients and users Pix. Moreover, institutions with over 500,000 active accounts are obligated to offer Pix.

- It’s safe. All users’ personal information is protected by the central bank secrecy and the General Data Protection Law.

- It promotes financial inclusion. Users do not need a bank account to pay with Pix.

- It’s cheap. Pix has a lower cost for companies than traditional TEDs or DOCs and is completely free for payers.

- It keeps adding functionality. The new options PIX Saque and PIX Troco allow users to withdraw cash from one of the points that offer the service (bakeries, department stores, supermarkets, ATMs, etc).

- It promotes e-commerce growth. Brazilian e-commerce is expected to grow 30% by the end of 2022. Meanwhile, Brazil’s population is becoming more and more mobile-centric, meaning that the majority of online shopping and payments would be made with the help of convenient mobile solutions such as PIX. PIX volumes for online purchases are expected to nearly double every year, growing at a 95% rate by 2024, with PIX potentially capturing at least 9% of the total Brazilian e-commerce volume.

At the same time, the speed and convenience of transactions pose certain risks to PIX users. The main issue connected with this popular payment system is so-called “lightning kidnappings”. When cash was the king, robbers used to threaten people in the street to force them to give away money from their wallet or withdraw it at the nearest ATM. Now, everything is simpler. People are grabbed on the street and forced to transfer money in exchange for their release. Although PIX transactions are traceable, robbers manage to use accounts or digital wallets of other people.

In the first six months of 2021, São Paulo has seen a 40% rise in such crimes. In response, the central bank has put a $200 transfer limit on P2P payments between 8pm and 6am, when most attacks occur. In addition, there is now a minimum waiting time for increasing transfer limits and people can choose to set their own different limits for day and night.

Nevertheless, the Legislative Assembly of São Paulo still proposed a law that would “suspend” Pix until the central bank implemented new security measures and has recently voted to fast-track this legislation. The proposed ban would be exclusively tied to the state of São Paulo, though.

SEE ALSO: